Friday, 23 February, 2024

Where mortgage stress is on the rise

Where mortgage stress is on the rise

For all the back-slapping about the absence of a recession and assuredness around a soft landing, this cycle is not yet over.

Christopher Joye Columnist

This column has been banging the table relentlessly about the fact the path for global services inflation will determine what happens to asset prices in 2024. The argument has been that most of the improvement in the inflation pulse has been an artefact of temporary goods deflation, which cannot continue in perpetuity.

The attenuation in inflationary pressures has been responsible for triggering the risk rally and expectations of early interest rate relief. Yet once the supply chain normalisation process is exhausted, and goods deflation desists, core inflation could increase sharply again as a result of elevated services inflation, where the latter is being driven by tight labour markets and robust wage growth.

During the week, dovish market participants were shocked by an extremely strong US inflation print characterised by an awkward combination of rebounding services inflation counterbalanced by accelerating goods deflation. US 10-year government bond yields surged above 4.3 per cent, having slumped as low as 3.8 per cent in January, which dragged the S&P 500 down almost 2 per cent in the session.

Needless to say, dovish communications from a US Federal Reserve board member have since convinced equity markets to claw back most of these losses while 10-year yields have remained relatively high at 4.23 per cent. Cognitive dissonance between bond and equity market signals has been a constant in recent times.

Very timely core US inflation rose 0.4 per cent in January, which pushed the three-month annualised pace up from 3 per cent in October to 3.6 per cent. On Coolabah’s analysis, the annualised trend in core inflation has climbed from 3 per cent to 4 per cent, which implies that the Fed’s task of securing sustainable price stability – as proxied by inflation around 2 per cent – remains exceedingly challenging.

What was most disconcerting for investors were the underlying influences on these numbers. Supply-side-affected core goods prices fell even faster in January, declining 0.3 per cent, elongating a sequence of declines in almost every month over the past year. On an annualised trend basis, goods deflation is running at about 2.1 per cent.

Advertisement

In contrast, demand-side-driven core services inflation actually accelerated, appreciating 0.7 per cent in January, the fastest pace since late 2022. On our trend analysis, annualised core services prices inflation has bounced from a low of 4.6 per cent in July to over 6.3 per cent, or from 3 per cent in May to 6.5 per cent if we remove housing costs.

A further worry is that the distribution of price changes suggests that inflation in the US is becoming more broad-based, with Coolabah’s estimate of the trend annualised change in “trimmed mean” inflation rising from 3 per cent in July to about 4.5 per cent in January.

Global cracks appearing

This was not part of the dovish script that has propelled asset prices higher since late 2023. Inflation was supposed to be mean-reverting towards 2 per cent. The hope was the Fed would start cutting rates in March and by a total of more than 150 basis points by the end of the year. At the time of writing, the first cut has been shifted to June and the totality of the cuts slashed to only 95 basis points this year. The spectre of a deferral of the start of the monetary policy easing process is something this column has repeatedly canvassed.

For the avoidance of doubt, the risk for investors is that US inflation, which is among the most timely data we receive globally, is a harbinger of the advent of secular stagflation. To confidently quell services inflation, the rapid growth in labour costs needs to be brought under control. All else being equal, this would normally require a meaningful increase in unemployment, which has failed to materialise.

For all the back-slapping about the absence of a recession and assuredness around a soft landing, this cycle is not yet over. We know that the global economy has been temporarily insulated from the impact of interest rate increases by the unprecedented cash buffers built up by consumers during the pandemic, which have now been mostly spent. In the US, this excess savings was equivalent to two years of additional economic growth.

Globally cracks are nonetheless starting to appear. On Thursday, the retail sales data in the US was much weaker than economists projected. New Zealand and the UK have reported negative GDP growth over the past 12 months, which would satisfy popular tests for a recession. January was the worst month for global corporate defaults since financial-crisis-affected 2010, according to Standard & Poor’s.

Notwithstanding the ostensibly strong features of the US economy – with a historically very low 3.7 per cent jobless rate, above-trend GDP growth and brisk wage inflation – 2023 was also the worst year for US corporate delinquencies covered by S&P since 2010 outside the pandemic-plagued 2020.

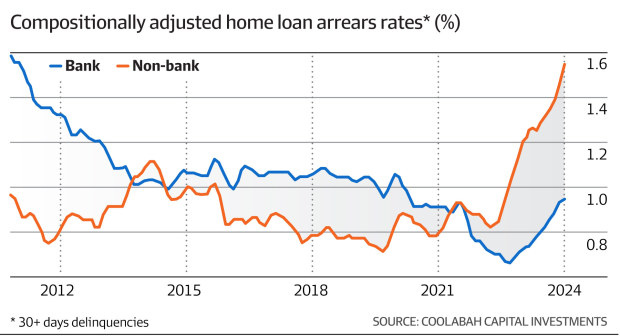

Non-bank loan stress

This insinuates that while many continue to do well, cyclically sensitive sectors are struggling. And that will only get worse if rate relief is deferred. Borrowers who predicated their finances and business models on the assumption of the availability of persistently cheap money are increasingly in serious strife.

We are seeing this start to resonate especially clearly in the Aussie home loan data. While house prices are appreciating and many feel more confident about their prospects, mortgage stress in the tails of the risk distribution is rising at an alarming rate.

Coolabah’s systems automatically track delinquencies on all securitised home loans issued by banks and non-banks. Whereas bank arrears have only risen modestly, stress in the non-bank lending space is a different matter. The 30-day delinquency rate on non-conforming or sub-prime loans has risen from around 2.5 per cent to circa 4 per cent. If we examine the higher-quality “prime” loans written by non-banks, the 30-day arrears rate has more than doubled from about 0.7 per cent to 1.6 per cent. This compares poorly with the change in arrears on the banks’ prime loans, which has crept up from 0.7 per cent to 1 per cent.

If you look back through history, you find that there have, in fact, been benign economic periods when the prime loans issued by non-banks have reported arrears rates that were slightly lower than those on prime bank loans. This might lead one to the spurious conclusion that prime non-bank loans were of comparable quality to prime bank loans.

The Trump factor

Yet we have seen that during any stress events – such as March 2020, or the period since the Reserve Bank of Australia started lifting rates in May 2022 – there is a striking bifurcation in the credit quality across unregulated non-bank lenders and heavily regulated banks that are subject to arguably the toughest prudential regulation in the world.

To conclude, I want to leave you with one final constructive thought. Experts assert that Donald Trump is likely to become the next US president. Trump is campaigning on a platform of much tougher immigration rules and the threat to slap yet more tariffs on China.

We discovered during the pandemic that starving tight labour markets of migrants is a recipe for strong wage inflation. We also know that tariffs are, by definition, highly inflationary. At a time when the US is struggling to dampen rampant services inflation driven by robust growth in labour costs, Trump could, once again, prove to be a toxic curveball for markets to contend with. Investors should, therefore, approach the next 12 months with a very open mind as to the distribution of potential paths for asset prices.